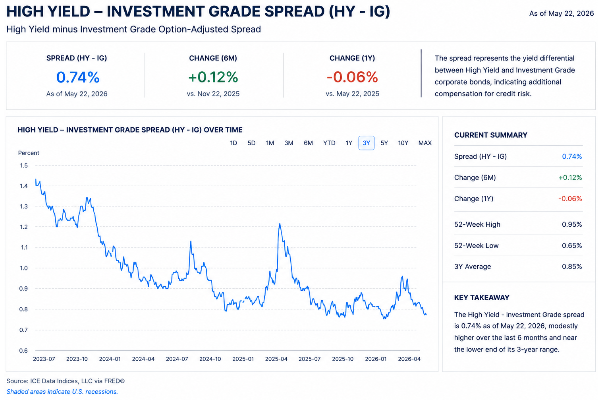

Credit Relative Value Performance

Credit Relative Value performance seeks to generate returns through the relative behavior of credit markets rather than relying solely on broad market direction. The strategy focuses on identifying periods where pricing between high-yield and investment-grade credit diverges from underlying macro and funding conditions.

Performance is expected to be driven by:

• Relative spread compression or expansion

• Shifts in risk appetite

• Credit market positioning

• Changes in financing conditions

• Temporary pricing dislocations across credit markets.

The objective is not to predict absolute market direction. The objective is to identify opportunities where relative pricing relationships become inconsistent with observed credit conditions.

The strategy aims to provide:

• Lower dependence on outright market direction

• Diversification relative to traditional long-only exposures

• Risk-adjusted returns through relative pricing opportunities

• A repeatable process centered on credit behavior and market structure

Performance evaluation emphasizes:

• Risk-adjusted returns

• Drawdown control

• Relative spread behavior

• Consistency of process execution

Success is measured not by predicting markets, but by maintaining a repeatable process that extracts value from credit dislocations over time.